.avif)

Published September 17, 2021

The Role of the Space Economy in InsurTech

Learn more about the space technologies that have made a significant impact on the insurance industry.

Learn more about the space technologies that have made a significant impact on the insurance industry.

Technologies such as, geospatial Intelligence, GPS, and the Internet of Things (IoT) have already had a significant impact on the insurance industry., In fact legacy insurance systems are seeking to take advantage of these technologies before they are edged out by younger InsurTech competitors. But what are these technologies exactly and how have they driven innovations in the insurance industry? Space Capital provides the answers to these questions and deep-dives into the trends in the space technology-based InsurTech solutions.

Geospatial intelligence - a blessing of the space technology industry - refers to the systems which derive information from earth images to provide context and insights from both a human-centered and environment-centered perspective. These technologies are frequently provided by satellite imaging, and can be used to analyze and predict weather risk, counter fraudulent claims, and even redefine traditional insurance models (e.g., parametric insurance). GPS technologies provide information about the location and timing of certain events on earth. InsurTech can leverage GPS to establish risk zones for various climate phenomena, provide data on the speed of an insured automobile, and locate insured cargo. Finally, IoT technology involves any device which can connect and transmit information via the cloud. IoT technologies are critical for the digitalization of the InsurTech sector and vastly improve customer experience with insurance.

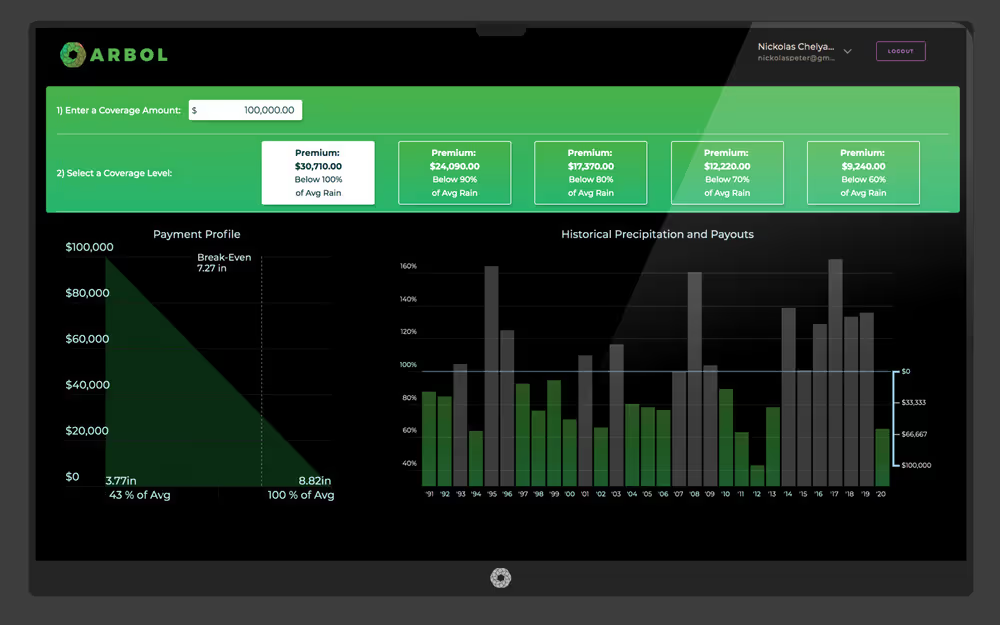

One of the most significant trends that has grown out of the collaboration between the insurance and space technology industries, or rather space technology-based InsurTech solutions is the growth of the nontraditional parametric insurance model. Under this model, a policyholder would receive an immediate payment of a pre-specified amount as soon as a trigger event covered by the insurance policy occurs. This model is particularly promising because it removes the human element from claims management, which decreases the time a policyholder has to wait for payment and removes the possibility of a fraudulent claim. Space Capital portfolio company Arbol makes use of the parametric insurance model for its climate and weather platform, saving the client from excessive broker fees that can cost up to 30% of the premium the client would pay under their old insurer. In conjunction with the parametric insurance model, Arbol uses a smart contract to automatically enforce the terms of the policy, which enables a quick payout to the policyholder. Because Arbol leverages satellite imagery to relay information about weather conditions and crop damages, there is no need for clients to file a claim. As soon as the trigger event occurs, satellites relay the necessary information to Arbol, and the company pays the client the pre-specified amount in under two weeks. Arbol is able to competitively price their product using thirty years of climate data to assess a company’s risk, given their location.

While Arbol focuses on agriculture clients from weather- and climate-related risks, other InsurTech companies have looked toward insuring either commercial or residential properties. Arturo, a Deep Learning spinout from American Family Insurance, leverages the innovations of the space technology industry by providing structured data about risks to residential and commercial properties generated from satellite and ground-level imaging. Geospatial data is able to determine the number of stories, the roof condition and contouring, and the positioning of commercial infrastructure including power lines and wastewater systems, allowing Arturo to build personalized risk profiles. Because our external environment is ever-changing when it comes to weather risk, and homes may either be renovated or deteriorate over time, satellite data allows the insurer to continually update these risk profiles instead of relying on decades-old data.

In the event that a property’s risk profile changes, InsurTech solutions can proactively identify the risk and share methods to mitigate damages before they occur. Delos is one example of a company engaging in proactive risk management. Delos is a property insurance Managing General Agent (MGA) which provides coverage for homes that are prone to climate disaster. One of their achievements is the creation of an ultra-precise model to identify low-risk homes in previously-considered high-risk areas for wildfires in California. Their models are built using large amounts of data including remote sensing imagery, wind and weather data, and user-entered information. With advanced algorithms, Delos is able to provide coverage to California homes when older insurers either refused, or would only extend coverage for prohibitively high deductibles and premiums. In the event that satellite imagery reveals a change to a policy that increases their risk of wildfire (i.e. vegetation encroachment or a change in the physical structures surrounding a home), real-time alerts are sent to the homeowners with actionable steps to respond.

The space technology industry has helped spur yet another critical innovation in the insurance sector. Flooding is another major climate disaster that legacy insurance companies were tentative to insure under homeowner’s or property insurance policies. This is a tremendous market opportunity, as 70% of losses due to flooding are uninsured, leading to approximately $40 billion in annual losses. Beyond geolocation, flood damages are highly dependent on elevation, so proper flooding models need accurate elevation data for every inch of the insured asset. Furthermore, due to climate change and other environmental factors, historical data alone is not sufficient to build highly accurate predictive models. Two InsurTech companies, reThought Climate and Cloud to Street have begun to address these challenges. reThought is an MGA able to achieve the required level of accuracy by integrating multiple stochastic models, deterministic models, and real-time data to make flood predictions. Using advanced analytics, the company is able to provide more affordable insurance and reinsurance policies for flooding, particularly for commercial property, public infrastructure, and high net worth homes. Cloud to Street is an analytics company that uses satellites and advanced artificial intelligence to gain global coverage of the planet, even through clouds and over rough terrain. Their models have been adopted by the UN for relief efforts, and 17 national governments worldwide rely on Cloud to Street data.

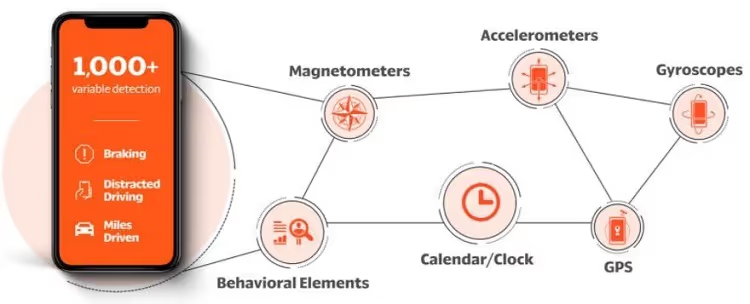

Root Insurance offers a GPS and IoT-based solution for auto insurance that personalizes the client’s rate based on how they drive. To determine the client’s risk, the client takes a test drive for a few weeks with Root app installed on his or her smartphone. Based on GPS data, the app analyzes the smoothness of braking, the speed at which turns are taken, whether or not the driver is following rules of the road (e.g., stopping at stop signs and abiding by the speed limit), and the driver’s driving patterns (e.g., the number of daily hours spent in the car along with what time of day the driver is out). Based on this test drive, Root insurance offers a personalized insurance policy to the client, which has the potential to save the driver up to $900 per year. Without the contributions of the space technology industry, this wouldn’t have been possible. Moreover, nearly every major auto insurance company is now offering a copycat product. Progressive’s Snapshot program uses either a tracking device that is plugged into the vehicle or a mobile app to track braking and acceleration patterns, daily time spent in the car, and which hours of the day are spent driving. Liberty Mutual, Allstate, Geico, Nationwide, State Farm, and USAA have also come up with similar programs.

Beyond addressing challenges in existing insurance sectors, space technology also enables insurance providers to grow into new sectors. One such sector that has seen tremendous growth and investment has been the marine and maritime industries. ScootScience is an underwriting firm whose goal is to “make oceans insurable.” Extreme temperature changes year over year, as well as changes in salinity, oxygen levels, algae blooms, and plankton concentrations, can lead to extreme losses to the aquaculture (fish farming) industry. ScootScience uses satellite and IoT data to allow fish farmers to choose the amount of protections they wish to receive in the event of a loss due to environmental changes. PAXAFE is a logistics insurance company focused on cargo as it traverses the oceans, rails, and roads to reach its final destination. In the past decade, cargo insurers have paid out more in claims than they have collected in premiums due to poor risk models and failure to track assets in real-time. PAXAFE has two products called Track-x and Sens-x which measure humidity, temperature, impact, light, and can track real-time asset location. These products send alerts to the user’s phone or computer about potential threats to shipments.

With a core competency in sourcing and evaluating early-stage investment opportunities, Space Capital ensures a diverse and profitable portfolio of the most promising, cutting-edge companies developing space technology that makes a big impact in the world. At the forefront of innovation in the space technology industry and economy, these companies have an enormous potential for growth. Check out our Technology Portfolio!

Check out Part 3 here.